Does your home need updating to sell, but you don't want to do the renovation? We have cash buyers who will buy your home!

Nearly 4 out of every 10 homes are owned "free and clear", in other words they are living without a mortgage, according to a study performed by Zillow. The state with the highest percentage of mortgage-less homes is West Virginia, which comes it at 54%. Conversely, Maryland and the District of Columbia ranked among the lowest with 27% and 24% of their homes being mortgage-less, respectively. Our state of California has roughly 29% of the homes owned free and clear.

Typically states that have a lower cost of living and lower home values will tend to have more homes owned free and clear.

On average Americans will stay in their homes 5-10 years, which is usually long enough to build up some decent equity, before selling the home and moving into what is usually a bigger home. In recent years with the lack of inventory and increasing prices, this number has been increasing. This also helps with increasing the amount of mortgage-less homes.

If you are like me and are already in your "forever home", or you are currently looking for that forever home, and you want to help grow that 40%, you're in luck! According to the study, over the past 10 years the percentage of Americans who have paid off their mortgage, has risen over 5%!

With a typical mortgage being 30 years, it can take a LONG time to get mortgage-free. Luckily for you, we have some tips to help you pay off your mortgage early.

One thing to note is that paying off your mortgage will have tax implications. If you have any questions as to how living mortgage free will impact your taxes, it is best to consult your favorite tax accountant.

Table of Contents

One option is dividing your monthly mortgage payment in two and paying that every two weeks. For example, if your monthly payment is $4,000 and you pay $2,000 every two weeks, you end up paying $52,000 instead of $48,000.

Because of there being 52 weeks in a year, you end up making 26 payments this way, which is the equivalent of 13 monthly payments. Plus once you get into the "groove" of making these payments, you shouldn't see much of an impact on your budget.

The one thing to make note of with this or any of the below methods, is to write "extra payments towards principal" on your checks. If you do not write this, the bank will usually put the extra money towards a future payment.

This is the tactic I personally use. Back when I was growing up, interest rates were in the mid to high teens and if you made one extra principal payment each year, you could cut your mortgage in half! A couple years ago I did the math on this to see if it still held true. Unfortunately, in the age of 3%-5% interest rates, it does not. Now I would need to make around 4 extra payments per year to see that desired effect.

The way loans are amortized, in the beginning years of your loan, your payment goes almost entirely towards interest and very little goes towards principal reduction. As time progresses, the percentage of your payment that goes towards interest decreases and the percentage that goes towards principal reduction increases.

As you pay down the principal, the amount of interest being charged becomes less (3% of $400,000 is greater than 3% of $325,000). Feel free to find a rate calculator, I personally use the one at Bankrate.com, and check out your own mortgage. You may find a significant savings on interest, depending on how new your loan is. On the "Amortization Schedule" tab, you can play with different options to see how an extra monthly payment versus annually, or no extra payments will impact your loan payoff

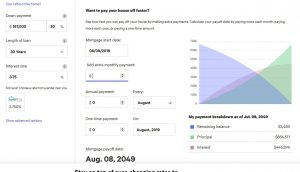

Using a recent sale of mine of $835,000 as a sales price, with 20% down and a 3.75% APR interest rate my payoff date is in 2049 and I'll be paying $444,000+ in interest. By paying $500 a month against the principa l, my payoff is in 2042 and I pay about $333,000 in interest. That's around a $111,000 savings in just 7ish years! That's Ferrari money!

l, my payoff is in 2042 and I pay about $333,000 in interest. That's around a $111,000 savings in just 7ish years! That's Ferrari money!

One important thing to note, not all loans allow you to make extra payments. Some have what is known as a "pre-payment penalty", which is something you should look out for and try to avoid when getting a loan. Some penalties may only apply to the first few years of the loan (where the bulk of the interest comes from).

Another great option to shorten your mortgage term is to ACTUALLY SHORTEN IT by changing from a 30 year loan to a 15 year loan. Now, while you can't just call up your bank and say "I want a 15 year loan now", what you would have to do is to refinance your home into a 15 year loan. If you need or want to make some more costly updates to your home (like a new kitchen), you may be able to pull some money out of your home at this time too. Just note that this will increase your loan balance and will require equity in your home.

One of the most frequently given piece of advice for anything financial from saving to buy a home, to paying off credit card debt, even to investing in stocks, or buying a new car is to reduce your expenses. I personally like to refer to your expenses as your "cost of living", since that is the term used by the government and statisticians.

While it may be a hard pill to swallow, I know I've done it, there are often some very easy and cost effective ways to save by reducing your cost of living.

Some examples are:

one more meal per week to work. You can actually make a healthy meal for less than many fast food (McDonalds) or casual dining (Applebee's) type restaurants and you don't have to tip! Example: I bought two beef kabobs and a Caesar salad for less than $10. At Outback that would be $16-$18 and would have much less salad. Add on tax at a higher amount and a 15% tip and you're looking at paying over double for less food!

one more meal per week to work. You can actually make a healthy meal for less than many fast food (McDonalds) or casual dining (Applebee's) type restaurants and you don't have to tip! Example: I bought two beef kabobs and a Caesar salad for less than $10. At Outback that would be $16-$18 and would have much less salad. Add on tax at a higher amount and a 15% tip and you're looking at paying over double for less food!If you look further into all your expenses, you can find things that you can cut down on or eliminate and every penny saved can be put towards your loan principal and really make a HUGE difference.

If you have more questions or need direct advice about what you can cut out, you can always meet with an accountant or a good friend.

If you liked this article, comment below and share it with your friends and family. Also feel free to check out our other blogs.